The Financial Conduct Authority announced the transition from the London Interbank Offered Rates (LIBOR) to Risk-Free Rates (RFRs) by year-end 2021. While banks will be able to submit LIBOR until the deadline, the transition will cause a considerable ripple effect within the global economy, with sweeping changes that will need to be made within the next two years. Financial institutions, investors, and legal counsel will need to assess their documents’ dependency on this reference rate and start developing alternatives in preparation for this significant impending market shift.

This will be a considerable challenge to tackle. Thankfully, legal tech has powerful digital tools that will prove invaluable as firms and corporations tackle the big changes needed during the transition.

What Are IBORs and What Do They Do?

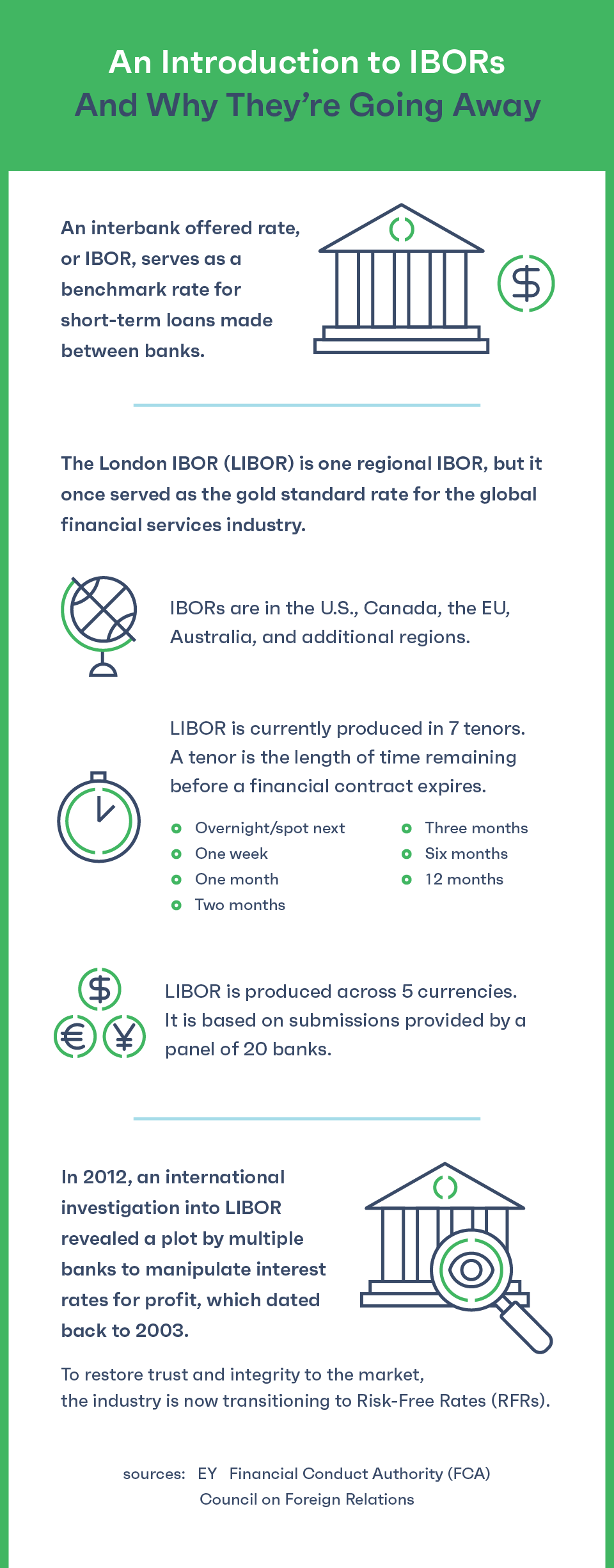

Interbank Offered Rates (IBORs) serve as a benchmark rate for short-term loans made between banks. A group of large, globally active banks submits their rates on a daily basis, which are published and serve as the foundation for the trade of several currencies and loans.

LIBOR is the gold standard rate for the global financial services industry. It is typical for loan contracts, securities, and derivates to reference LIBOR rates as an integral part of their agreements. In fact, it is estimated that there are over $400 trillion of wholesale and consumer global contracts that have defined their reference rate by LIBOR submissions.

Why the Switch?

This landmark decision to transition to Risk-Free Rates (RFRs) is due to a focus on restoring trust and integrity in the market. This shift comes after several cases of misconduct involving banks' LIBOR submissions. The decision to nix LIBOR has triggered a global movement away from IBORs, such as:

- CDOR in Canada

- BBSW in Australia

- EURIBOR in the EU

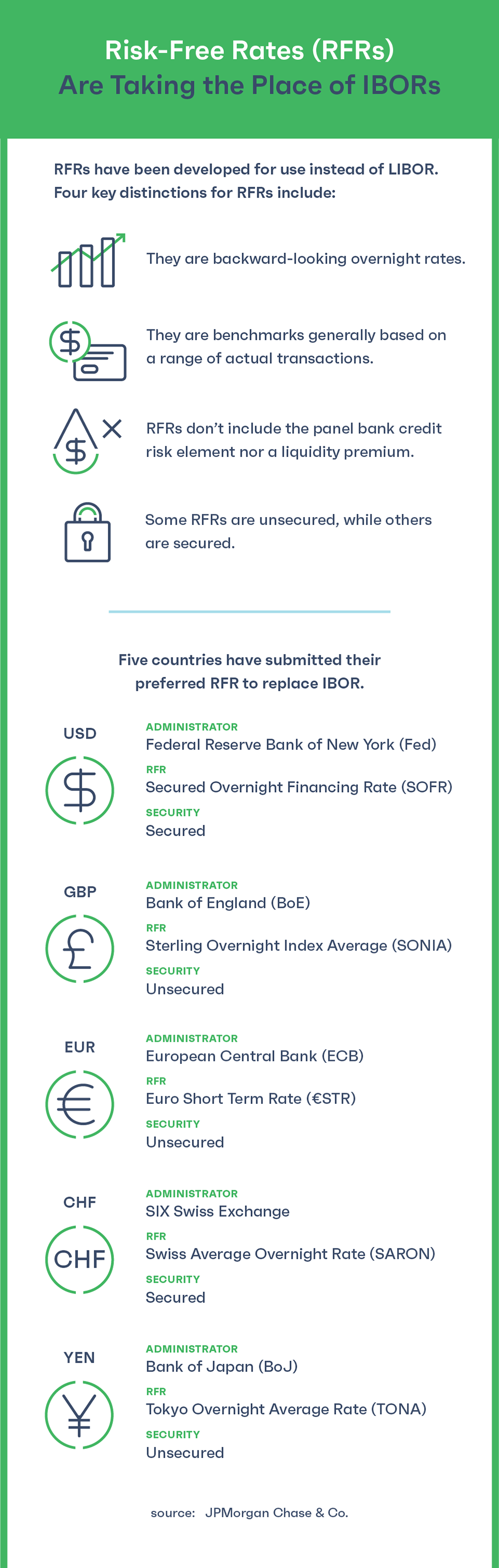

Countries have begun the transition away from IBOR toward other, alternative reference rates. In order to protect future transactions from manipulation, banks will be transitioning to these alternative reference rates based on overnight RFRs that are anchored in sufficiently liquid money markets. There are currently five countries that have submitted their preferred RFR to replace IBOR.

What Are the Differences Between RFRs and LIBOR?

The LIBOR benchmarks are forward-looking term rates based on submissions by banks that estimate the borrowing of funds in the future. RFRs take current data of transactions that have already occurred, providing a more accurate current picture of the economy.

LIBOR contains a higher implied credit risk that is aligned with the length of a given interest period. RFRs don’t have any premium or credit risk because of their short-term nature as overnight rates. The United States' RFR, Secured Overnight Financing Rate (SOFR), is secured, while other RFRs are not.

It is anticipated that the switch to RFRs will be a bit chaotic at first. LIBOR offered central management of multiple currencies. Each country’s RFRs will contain different characteristics that could have confusing consequences, such as multiple rates co-existing depending on the government, industry, or market. However, specific institutions can provide guidance with alternative credit-sensitive benchmarks that can give a close match to existing marginal funding costs, allowing RFRs to fulfill niche market needs.

It is crucial that financial intermediaries and their legal counsel, especially those dealing with international transactions, are informed on how the IBOR transition can impact existing contracts and documents. They should begin preparations to minimize any potential future implications.

What Are the Potential Impacts of an IBOR Transition?

While the transition from IBORs to RFRs won’t be complete for some time, the potential impact is already being felt across global markets as institutions scramble to review, amend, and research impending changes. The Bank for International Settlements, one of the world’s oldest financial institutions, described the IBOR transition as “akin to surgery on the pumping heart of the financial system.”

Extensive Expenditure of Time

Large commercial organizations are faced with the daunting task of identifying and reviewing a high volume of documents related to the IBOR transition. Investment funds or other commercial entities that deal with large debt transactions are scrambling to determine which contracts have sufficient fallback terms in place and which need to be repaired, and are contacting clients to notify and request amendments. Both parties need to have a high-level understanding of the impact of alternative RFRs, as well as how to mitigate any conflicts and share the transition costs.

Other complex considerations may be affected by the IBOR transition, such as:

- Maturity dates

- The firm’s role in the contract

- Benchmark uses

- Any jurisdictional concerns for governing law and possible litigation

Identifying potential risks and roadblocks, as well as revisiting these terms with clients, will take considerable time, especially in the high-volume commercial contract environment.

The Burden of Cost

Especially in the United States, LIBOR has been the go-to reference rate for more than 40 years. It’s been used as the standard in hundreds of thousands of documents dealing with investment, loan, and debt transactions. The legal costs of review, negotiation, and amendment are immense. It is estimated that legal and contract remediation for the IBOR transition may cost more than $50 million.

While some contracts may have an already established a fallback rate, it may not be an attractive option compared to another RFR that was not yet available when the borrower created the contract. According to EY Americas, fallback provisions were designed in the event of the temporary unavailability of LIBOR, not a permanent elimination. They are often written vaguely or lack clarity, which could produce long-term adverse financial outcomes. For example, if one presiding financial institution determines their own approach to RFRs, clients could be negatively impacted, leading to real losses and contractual issues without a clear solution. If negative financial impacts were to occur due to a transition to RFRs, firms and banks will need to establish who will shoulder the cost and the extent of the financial burden.

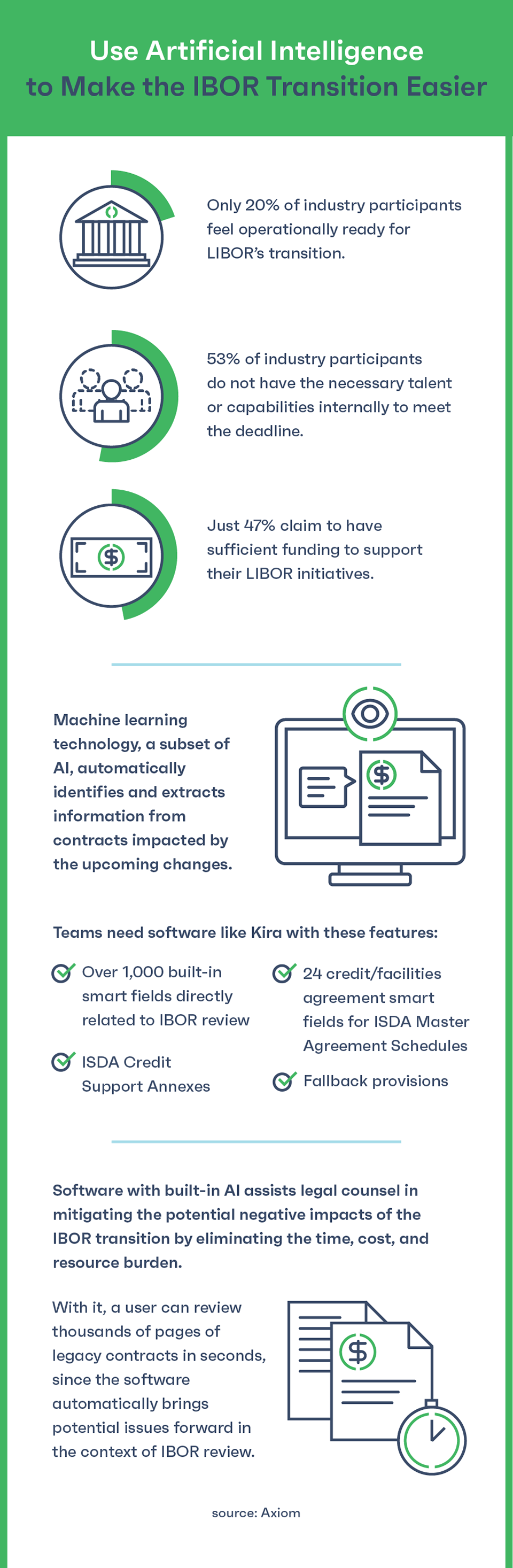

Amendments will be necessary, but the cost to negotiate and amend will be significant. Only 47% of the impacted companies and contracting parties report that they have sufficient funding to deal with the transition. This has led firms to seek more affordable solutions for IBOR review.

Enormous Resources

The fluctuations in the global economy have limited many financial industries’ and firms' resources, requiring legal teams to do more with less. In a recent survey, almost 50% of consumers said they would delay seeking legal help until after the COVID-19 pandemic. Reduced revenue has caused a ripple effect, and layoffs in Big Law have begun to impact the efficiency of large corporate clients. Many paralegals and new associates have been cut or given a delayed start date, and lawyers are finding themselves with endless billables and little support.

The transition away from IBOR will take an enormous amount of legal resources from the initial term discovery through negotiation, repapering, and client outreach. It is imperative that legal counsel for clients managing an IBOR transition put together a comprehensive strategy that makes the most out of their time. This may be challenging given the pandemic and staffing concerns that will likely extend for the foreseeable future.

Thankfully, there are digital solutions that can ease the burden for in-house counsel, firms, and corporate clients alike. These solutions have a powerful tool: artificial intelligence.

How Artificial Intelligence Will Assist with the IBOR Review Process

With only 20% of industry participants feeling prepared for the LIBOR transition, it is no surprise that leaders are looking for assistance in this herculean task.

Kira Systems has an unmatched machine learning technology that automatically identifies and extracts information from contracts impacted by the upcoming changes. It comes with over 1,000 built-in smart fields directly related to IBOR review, fallback provisions, 24 credit/facilities agreement smart fields for ISDA Master Agreement Schedules, and ISDA Credit Support Annexes.

Occasionally contracts contain unique identifiers or unusual information. Kira Quick Study is a proprietary feature that allows users to create their own smart fields to spot specific provisions, terms, clauses, or data points within a contract. The entire user interface is intuitive and requires no coding, AI expertise, or computer-learning knowledge.

Artificial intelligence assists legal counsel in mitigating the potential negative impacts of the IBOR transition by eliminating the time, cost, and resource burden. Clients are granted a high-level understanding of how the impending transition will impact their existing contracts. Kira quickly identifies potential issues and can export summaries of essential provisions. With Kira, a user can review thousands of pages of legacy contracts in seconds, since the software automatically brings potential issues forward in the context of IBOR review.

Artificial Intelligence Makes the IBOR Transition Easier

From the announcement of the LIBOR transition in early 2019 through to the global pandemic, the last few years have been a test of strength for many companies, corporations, and firms. However, these challenges have brought an appreciation for the digital tools that can help legal firms deliver efficiency that was previously thought to be impossible. Just a few years ago, an IBOR transition would have been backbreaking to a multitude of clients. By utilizing software equipped with artificial intelligence, clients can quickly gain insight and control over IBOR review, making the transition a challenging, but completely manageable process.