When times get tough, loans can be a critical resource to help companies weather a storm. More specifically, credit facilities can be real life savers. This type of loan is a lending institution’s offer to extend credit to a business client, often in the form of overdraft services, revolving lines of credit, or letters of credit. The credit agreement is a written document that spells out the terms of the loan.

While the financial institution usually prepares the first draft of the agreement, it is subject to negotiation. A prospective borrower should have a clear overview of what it wants from the credit facility. Read on to learn about different types of facilities as well as common credit agreement provisions.

Credit Facility

A credit facility is an offer of financial assistance made by a financial institution to a company. A document called a credit agreement, facility letter, or loan agreement details the terms. The lender initially prepares it — often in the form of a letter — but the borrower can negotiate the terms.

Common Credit Agreement Provisions

Most provisions of a credit agreement are drafted to meet the situation. However, credit agreements often include some common provisions. These include provisions describing the following.

Type/nature of facility

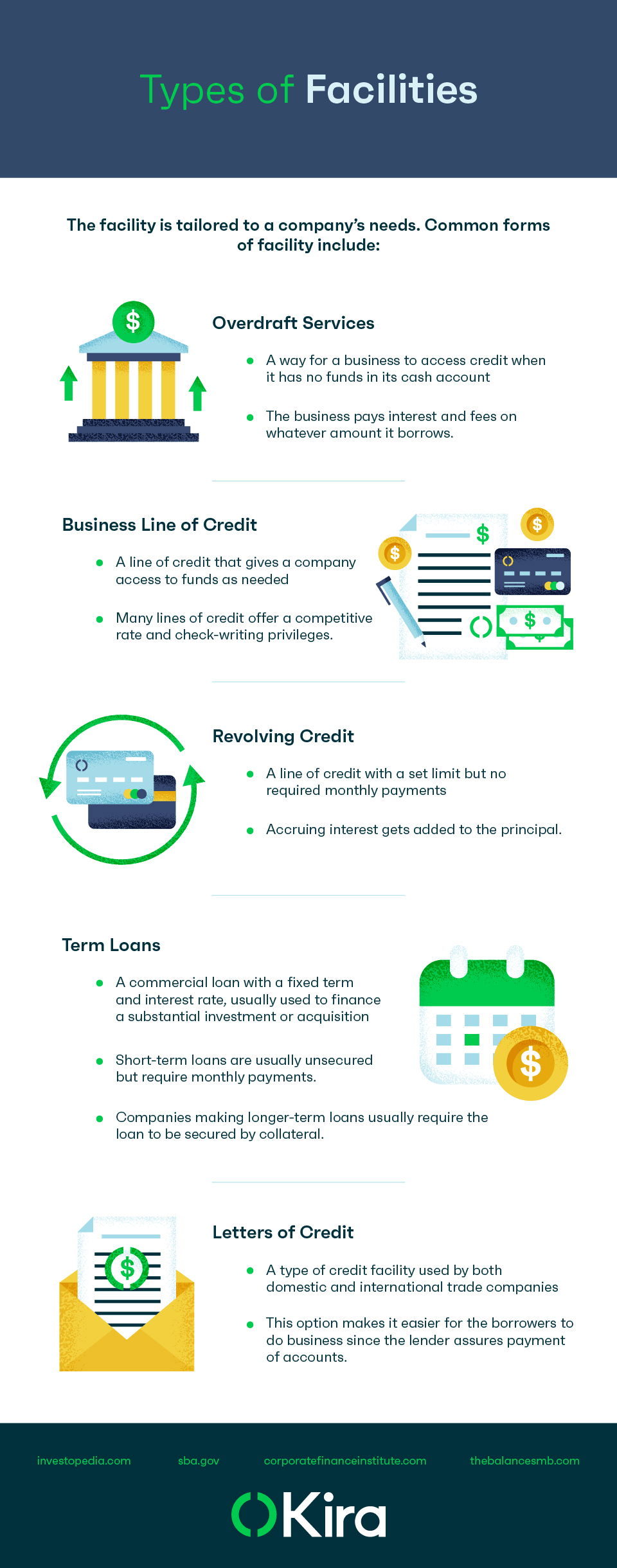

More than one facility, committed or uncommitted, can be included in a credit agreement. Committed means that the lender is obligated to make the loan once the borrower has satisfied any conditions precedent (meaning a condition that must be satisfied before the loan is issued). Uncommitted means that the lender is not obliged to make the loan and is usually reserved for short-term loans.

Amount of facility

This means the maximum amount that the financial institution will lend.

Secured or unsecured

A secured loan is one in which the borrower offers collateral as a guarantee that the loan will be repaid, effectively lowering the lender’s risk. For example, real estate is routinely used as collateral to secure a real estate purchase loan. Some credit facilities are secured, but many are unsecured.

Purpose of facility

While not every facility agreement requires the loaned money to be used for a specified purpose, most do. Lenders prefer to specify the purpose to be sure it lines up with the lender’s credit analysis.

Interest

The interest clause sets out the interest rate on the loan. Interest rates can be fixed (a specified rate that doesn’t change) or variable (based on an interest rate margin added to a benchmark rate, like the benchmark rate plus 3 percent).

Covenants, representations, and warranties

These provisions describe the different promises and representations the parties have made to one another. It also lists any exceptions to those promises. It’s very important to review covenants carefully since, according to our recent study, a significant number of credit agreements are drafted in a manner that allow the borrowers to shift assets intended to serve as collateral out of the grasp of lenders.

Events of default

An event of default is an act or omission that puts the borrower into default, such as failure to make a required payment or breach of a term of the facility agreement. If the borrower has multiple facility agreements with the lender, a cross-default provision provides that a default of any facility constitutes a default of all.

Other costs, fees, and payment obligations

This provision includes any prepayment fees that the borrower owes if they repay the facility earlier than the time specified.

Definitions

This provision defines various terms used in the agreement to make sure all parties get on the same page.

Interpretation of provisions

This provision sets out the parties’ understanding of agreement terms in case there is an issue.

Mechanics of borrowing and repayment

The repayment provision details whether the borrower repays the facility on a fixed date or schedule, or whether they must repay it on demand.

Boilerplate provisions

This is the term given to standard provisions included in every facility. For example, a provision that written agreement is necessary to modify the terms of the loan may be part of the boilerplate.

Schedules

A conditions precedent schedule sets out any conditions precedent. For example, a condition precedent might be a requirement that the borrower sign an agreement to take all disputes over the contract to arbitration.

Kira for Finance

Understanding what’s in an organization’s credit agreements can be time-consuming. However, Kira makes the process easier with state-of-the-art machine learning contract analysis technology which identifies and extracts information from contracts and other documents. It comes with 190 credit/facility agreement smart fields, more than 100 ISDA smart fields, and more than 40 commitment letter smart fields. Plus, Kira’s new Answers & Insights technology interprets the extracted data to provide businesses with instant answers to pressing questions.